There are various crypto portfolio composition approaches for investors looking to invest in the global crypto markets, each having performed differently during the bull market of 2021 and the bear market of H1/2022.

Read on to learn about the most popular algorithmically-managed crypto portfolio compositions and how they have performed in different market scenarios.

Our Investment Universe for this Study

To study crypto portfolio composition, we have retained a ten coins portfolio.

The ten crypto assets are BTC, ETH, BNB, LTC, XRP, SOL, ADA, AVAX, DOGE, and LUNA. We chose this universe of cryptocurrencies to have strong performing coins, laggards, and coins that performed very well but for a short period of time in the blend while maintaining the number of coins relatively small to observe the effect of the LUNA crash at the end.

The Goal of Portfolio Building Algorithms

When you want to build a systematic portfolio, you have several options.

The simplest way is to weigh an asset by the function of its market capitalization (Market Cap Weighted Portfolio). Without token creation or burns, airdrops, or forks, this type of portfolio doesn’t need rebalancing.

You can also try to minimize the final risk. This kind of portfolio is called a Minimum Variance Portfolio.

Alternatively, you can try to play with diversification, and the simplest way to do that is to allocate the same budget to each token (Equal Weighted 1/n portfolio).

Finally, you can try to manage your portfolio’s risks while adding some diversification, and that is the goal of the risk parity algorithms. These algorithms use the correlation matrix as it describes inter-coin relationships.

The crypto world is still very young, and contrary to traditional markets, the correlation matrix describes a universe where cross-correlations are very high.

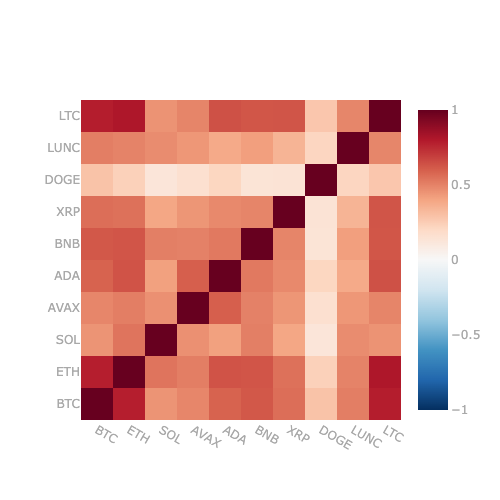

Correlations between 01/01/2021 and 01/05/2022

For our portfolio composition study, we plotted the daily correlation matrix between 01/01/2021 and 01/05/2022 (just before the collapse of LUNA), and we can observe that in that period, except for Dogecoin (DOGE), the correlations between the different tokens are between 40% and 80%. This means that it is complicated to extract some diversification and that it is a challenging environment for optimizers where we should face some instability.

Types of Crypto Portfolio Compositions

Let’s take a look at the most common portfolio composition approaches in the digital asset markets.

Market Capitalization Weighted Index

In a market capitalization-weighted crypto portfolio, the weight of a token holding in the portfolio is determined by the market cap of this token compared to the sum of the market caps of all tokens in the index. Most leading stock indices, like the S&P 500 or DJ EuroStoxx 50, for example, use this composition approach.

Equal Weighted Portfolio (1/n)

An equally-weighted crypto portfolio holds the same percentage in each token It aims to achieve broad diversification. In our case we will rebalance daily at midnight UTC.

Minimum Variance Portfolio (MVP)

A minimum variance portfolio, as its name suggests, aims to algorithmically minimize the variance of the portfolio. Variance is the square of volatility.

Equal Risk Weighted (ERC) Portfolio

An ERC portfolio aims to allocate to each token the same quantity of risk, i.e., the risk contribution of each asset to the portfolio should be the same. This portfolio is between the Equal Weighted Portfolio (1/n) and the Minimum Variance Portfolio and is one of the most used portfolio composition algorithms.

For this portfolio, we used daily rebalancing at midnight UTC with a computation period of 90 days x 24 hours using hourly data.

Inverse Variance Portfolio (IVP)

An inverse variance portfolio will allocate each asset proportionally to the inverse of the variance of the asset. The variance is the square of the volatility. We can notice that this risk parity algorithm doesn’t take the covariance matrix into account.

For this portfolio, we used daily rebalancing at midnight UTC with a computation period of 90 days x 24 hours using hourly data.

Hierarchical Risk Parity (HRP) Portfolio

An HRP’s portfolio computation is more complex. It uses the Hierarchical Risk Parity algorithm developed by Marco Lopez de Prado in 2016. This algorithm uses graph theory and machine learning techniques to build a diversified portfolio without inverting the covariance matrix, which is a source of instability (especially in our case, as we saw before).

The first step consists of clustering based on the covariance matrix and the second in a 3/7 weight allocation in these clusters. Results given by the HRP algorithm tend to be more stable and robust than traditional risk parity algorithms.

How Have Different Portfolio Compositions Performed in the last Crypto Bull & Bear Markets?

Now, let’s take a look at how each of these portfolios performed during the recent bull and bear markets, ranging from 2020 to mid-2022.

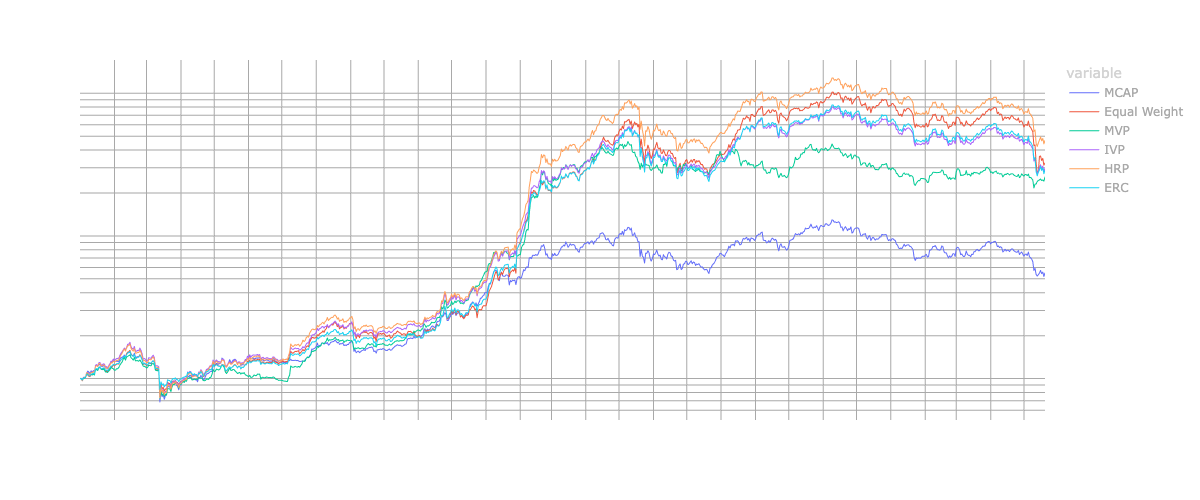

Portfolio Performance 2020 to 20/05/22

Looking at the performance of our model portfolios, we can observe that during 2020 and a bull run globally driven by Bitcoin (BTC), the different portfolios showed similar performances, while HRP, MVP, and IVP have outperformed slightly.

In 2021, during which the market witnessed a furious altcoin bull run, the story is different. All the portfolios, but especially the Hierarchical Risk Parity (HRP) Portfolio, strongly outperformed the market cap index.

In our asset universe, we chose some big winners of 2021 (DOGE, SOL, AVAX, LUNA) for this study. So an allocation that would allocate a substantial part of the portfolio to these assets would strongly outperform a portfolio mainly allocated to Bitcoin.

Nevertheless, we could anticipate an outperformance of the riskiest portfolio – the equal weight 1/n portfolio – in this particularly favorable environment. However, the HRP managed to clearly outperform.

We also note that the MVP underperforms the other risk parity models during the second half of the year as it fails to catch the summer rebound. However, it manages to capture the altcoins bull run in Q1/2021 and, in the end, strongly outperforms the market cap-weighted portfolio, even if it should be more defensive.

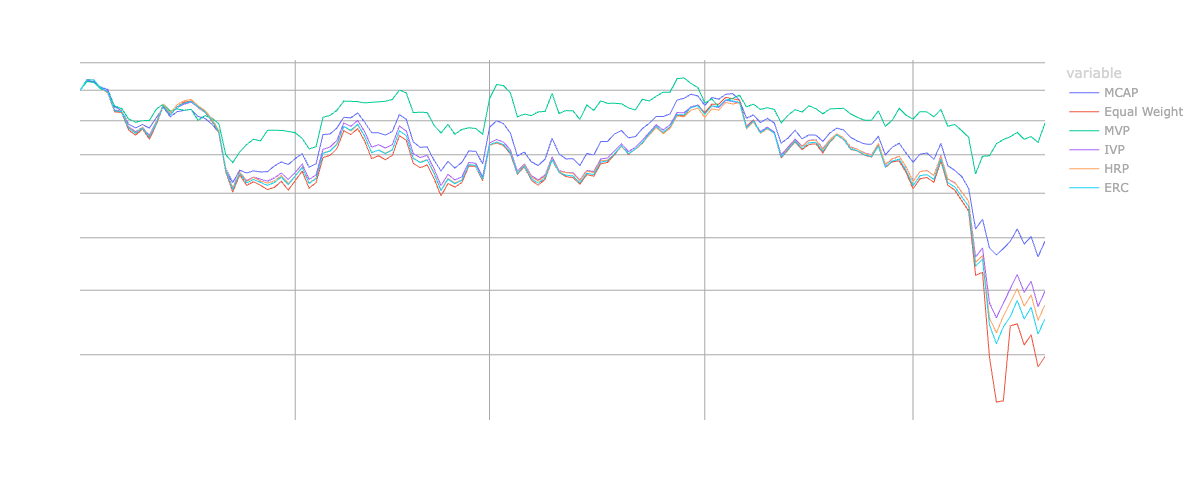

Zoom in on 2022

If we zoom in on 2022, we can observe how the different portfolio compositions have behaved during the bear market and following the crash of Luna.

We can notice that the MVP portfolio effectively minimized the risk and strongly outperformed the other portfolios. Then the market cap-weighted portfolio, with its greater allocation to the largest crypto assets by market cap, which could be seen as a defensive strategy during this phase, outperforms the other portfolios. We can notice that this portfolio won’t reallocate to LUNA during the crash, just letting the dedicated LUNA part go to zero.

Other portfolios have a bigger exposition to LUNA as they are more balanced, but also a rebalancing mechanism that could increase or decrease the exposure to LUNA.

On the one hand, the volatility or the variance will explode, so the associated risk, and we can be sure that the MVP portfolio will cut its exposure to it, and IVP will reduce it drastically. On the other hand, the allocation in percent of the portfolio has decreased a lot, and a rebalancing should increase the exposure.

In the end, we can notice that except for MVP, the IVP is the best risk parity performer (as it is the most sensitive to the increase of an isolated risk), followed by the HRP, then ERC, and finally the equally-weight portfolio that massively underperforms during the crash.

Bonus: KPIs of the Portfolios

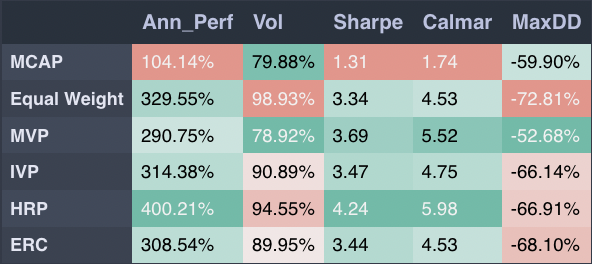

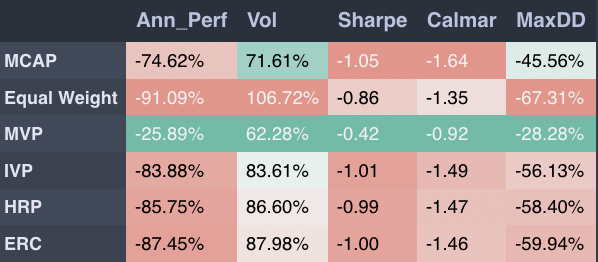

If you want to gain deeper insight into our model portfolios, you can view all the KPIs below for the period January 2021 to May 2022 and January 2022 to May 2022.

2021 – 05/2022 period

2022

Conclusion

In the long run, the market capitalization-weighted portfolio lags during furious bull runs because of its strong allocation to the biggest coins and resists well compared to the other portfolios during bear markets and extreme events (until these events concern Bitcoin or Ethereum).

On the other side, the HRP portfolio is one of the big winners. It outperforms during the bull run and resists relatively well compared to other risk parity portfolios in extreme events. It is, in reality, not surprising, that the efficiency of risk parity algorithms is conditioned by the stability of the covariance matrix, as most of them require an inversion of this matrix.

With a traditional portfolio, it is grosso modo the case as you generally assemble uncorrelated assets. But in the crypto world and until now, correlations between tokens are very high. This gives an advantage to this method, which doesn’t need a covariance matrix inversion and is generally more stable in its outputs.

Last but not least, we can notice the performance of an MVP portfolio that captures the best of the two worlds: it catches a strong part of the altcoins bull run and massively outperforms the market cap-weighted portfolio. Moreover, it also resists well in the bear market beginning in 2022 and finally strongly outperforms the other portfolios in the crash of LUNA.

To conclude, we could say that an HRP portfolio was the best to maximize its gains over the long-term period, and for low-risk profiles or a bigger sensitivity to drawdowns, the MVP portfolio did far better than the market cap weighted portfolio both in the furious bull run of 2021 and in the bear market of 2022.

This suggests that actively-managed, quantitative investment strategies will likely outperform the popular market capitalization-weighted portfolio in the digital asset markets.

Invest in Algorithmically-Powered, Tailor-Made Crypto Funds with Iconic

Active investment strategies enable fund managers to offer customized portfolios with clearly outlined risk and expected return parameters to their customers.

Iconic Alpha AG is the newly launched actively-managed crypto investment arm of Iconic, specializing in quantitative and algorithmic trading solutions.

Through a combination of long-short and smart beta strategies powered by proprietary trading algorithms developed in-house, Iconic Alpha offers Separately Managed Accounts (SMAs) to high-net-worth individuals and professional investors looking to gain exposure to the global crypto asset markets without the high volatility.

To learn more about Iconic Quantitative Solutions and how you can invest in an actively managed crypto fund, click here.

About Iconic Funds

Iconic Funds is the bridge to crypto asset investing through trusted investment vehicles. We provide investors both passive and alpha-seeking strategies to crypto, as well as venture capital opportunities.

We deliver excellence through familiar, regulated vehicles offering investors the quality assurances they deserve from a world-class asset manager as we champion our mission of driving crypto asset adoption.

Recent News and Articles

- How to Invest in Ethereum (ETH): A Guide for Professional Investors

- The Case for Actively Managed Investment Strategies in the Crypto Markets

- Iconic Launches Actively Managed Crypto Investment Platform with Recently Acquired Quantitative Solutions Team

- How to Invest in NFTs: A Guide for Professional Investors

- Bitcoin vs. Gold: Why You Are Probably Better Off Buying “Digital Gold”

- Why Bitcoin’s Volatility Shouldn’t Scare You

- How accurate is the Bitcoin Stock-to_Flow Model?

Iconic in Press

- ETF stream: White-label issuers in Europe quietly tripled in a week

- ETF strategy: Iconic Funds debuts world’s first ApeCoin crypto ETP

- Das Investment: Kryptowährungen kommen 2022 im Mainstream an

- Private Banking Magazin, Bitcoin – das perfekte Beispiel für ein ESG-Investment?

- Institutional Money, Krypto-Manager steigt bei Family Office ein

- Morningstar, Iconic Funds Expands Product Range With a Physical Ethereum ETP

Recent Research Reports

How did portfolios perform during the pandemic? ➡ Download here

Analyzing the Primary Value Drivers of Leading Cryptocurrencies ➡ Download here

How Effective are Common Investment Strategies with Bitcoin? ➡ Download here

Investigating the Myth of Zero Correlation Between Crypto Currencies and Market Indices ➡ Download here

For further information, please visit deutschedastg

Legal Disclaimer

The material and information contained in this article is for informational purposes only. Iconic Holding GmbH, its affiliates, and subsidiaries are not soliciting any action based upon such material. This article is neither investment advice nor a recommendation or solicitation to buy any securities. Performance is unpredictable. Past performance is hence not an indication of any future performance. You agree to do your own research and due diligence before making any investment decision with respect to securities or investment opportunities discussed herein. Our articles and reports include forward-looking statements, estimates, projections, and opinions. These may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Iconic Holding GmbH’s control. We believe all information contained herein is accurate, reliable and has been obtained from public sources. However, such information is presented “as is” without warranty of any kind.